1

Please refer to important disclosures at the end of this report

1

1

PSP Project Ltd. (PSP) is a multidisciplinary construction company offering a

diversified range of construction and allied services across industrial, institutional,

government, government residential and residential projects in India. PSP

provides services across the construction value chain, ranging from planning and

design to construction and post-construction activities to private and public sector

enterprises. Historically, PSP has focused on projects in the Gujarat region. PSP

has recently diversified its portfolio of services across geographies and is

undertaking or has bid for projects pan India. The company’s standalone total

order book as of March 31, 2017 was `729.2Cr, which comprised of 17

institutional projects, 4 industrial projects, 4 government projects and 2

government residential projects. Further, subsidiaries and JV’s have total order

book of `90.9Cr and `107.4Cr respectively as of March 31, 2017.

Positives: (a) Strong track record of successful project execution; (b) Long-standing

relationships with customers; (c) Leveraging position as a rapidly growing

construction company in Gujarat; (d) Augment customer relationships and

optimize project mix; (e) Expanding geographical footprint; (f) Experienced

management and promoter.

Investment concerns: (a) Historically PSP has executed ~70% of its total projects in

Gujarat except three which have been recently added (i.e. two in Rajasthan & one

in Karnataka); (b) PSP’s aspiration of getting in the higher value projects may not

capitalize as that space is highly competitive and dominated by bigger and

renowned players; (c) Current strategy of bidding for project of tenure 12-18

months leaves less visibility of future order book vis-à-vis future revenue growth;

(d) Margin profile may not be sustainable, as it is function of project mix; (e)Lack

of experience in different geographies may escalate the cost of project and

delivery.

Outlook and Valuation: In terms of valuation, PSP’s P/BV multiple annualised

9MFY2017 at 7.9x, works out to be at premium to peers (Ahluwalia Contracts

5.2x, Nila Infra. 3.3x, JMC projects 1.4x, Prakash Controwell 0.4x, RPP Infra

3.7x). Moreover, PSP is aspiring to get in the higher ticket size projects, which is

dominated by well reputed players. Management’s lack of experience in diverse

geographies and lack of visibility of future order book may become a cause of

concern for growth strategy. Hence, we recommend NEUTRAL rating on the issue.

Key Financials

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

9MFY17

Net Sales

257.2

210.4

280.5

476.0

278.5

% chg

44.0

-18.2

33.3

69.7

-

Net Profit

12.3

10.1

14.1

22.7

20.8

% chg

46.4

-17.7

39.4

60.8

6.0

OPM (%)

8.5

8.0

8.0

7.3

11.5

EPS (`)

4.3

3.5

4.9

7.9

7.2

P/E (x)

49.2

59.8

42.9

26.7

-

P/BV (x)

22.7

17.4

12.9

9.5

-

RoE (%)

46.1

28.9

30.0

34.2

-

EV/Sales (x)

2.2

2.6

1.9

1.1

-

EV/EBITDA (x)

25.9

33.0

24.1

15.0

-

Source: Company, Angel Research; Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

NEUTRAL

Issue Open: May 17, 2017

Issue Close: May 19, 2017

QIBs 75% of issue

Non-Institutional 10% of issue

Retail 15% of issue

Promoters 72%

Others 28%

Post Issue Sh areholdin g Pattern

Post Eq. Paid up Capital: `36.0cr

Issue size (amount): *`207cr -**212 cr

Price Band: `205-210

Lot Size: 70 shares and in multiple

thereafter

Post-issue implied mkt. cap: *`738cr -

**`756cr

Promoters holding Pre-Issue: 99.99%

Promoters holding Post-Issue: 71.99%

*Calculated on lower price band

** Calculated on upper price band

Book Bu ilding

Fresh issue: `151.2 cr

Face Value: `10

Present Eq. Paid up Capital: `28.8cr

Offer for Sale: **0.29cr Shares

Abhishek Lodhiya

+022 39357600, Extn: 6811

Abhishek.lodhiya@angelbroking.com

PSP Projects Limited

IPO Note | Construction

May 16, 2017

2

PSP Projects | IPO Note

May 16, 2017

2

Company background

PSP Projects is a multidisciplinary construction company offering a diversified range

of construction and allied services across industrial, institutional, government,

government residential and residential projects in India. Company provides

services across the construction value chain, ranging from planning and design to

construction and post-construction activities to private and public sector

enterprises. Historically, company has focused on projects in the Gujarat region.

PSP has recently diversified its portfolio of services across geographies and is

undertaking or has bid for projects pan India.

Over the years, PSP has successfully executed a number of prestigious projects

across Gujarat. One of the first major projects that the company had completed

was the construction of the GCS Medical College, Hospital and Research Centre

(managed by the Gujarat Cancer Society) in June 2012. Subsequently, PSP has

successfully executed a number of prestigious projects, including, Inter Alia, the

construction and interior works of Swarnim Sankul 01 and 02 at Gandhinagar,

Zydus Hospital at Ahmedabad, and various activities in relation to the Sabarmati

Riverfront Development project at Ahmedabad. Further, company has completed

or is currently undertaking projects for a number of reputed customers, including,

Inter Alia, Cadila Healthcare Limited, Care Institute of Medical Sciences Limited

(CIMS), Claris Injectables Limited, Emcure Pharmaceuticals Limited, Gelco

Electronics Private Limited, GCS Medical College, Hospital and Research Centre

(managed by the Gujarat Cancer Society), the Government of Gujarat (through the

Executive Engineer, Capital Project Division), Inductotherm (India) Private Limited,

Intas Pharmaceutical Limited, Kaira District Co-operative Milk Producers’ Union

Limited (Amul Dairy), KHS Machinery Private Limited, Nirma Limited, Sabarmati

River Front Development Corporation Limited, Torrent Pharmaceuticals Limited

and WTC Noida Development Company Private Limited.

Company’s execution capabilities have grown significantly with time, both in terms

of the size of projects bid for and the number of projects that it executes

simultaneously. Since incorporation in August 2008, PSP has executed 80 projects

as of March 31, 2017. Company’s Chairman and Managing Director and CEO,

Prahaladbhai Shivrambhai Patel, who is also a Promoter, has been associated with

the construction business for over 30 years and has been instrumental in the

growth of Company.

PSP Projects has two subsidiaries namely PSP Projects Inc. (USA, 100%) and PSP

Projects and Proactive Constructions Private Limited (74%), and a joint venture

between GDCL & PSP where company’s economic interest is 49%. P & J Builders

LLC is a step down subsidiary of the PSP Projects Inc.

3

PSP Projects | IPO Note

May 16, 2017

3

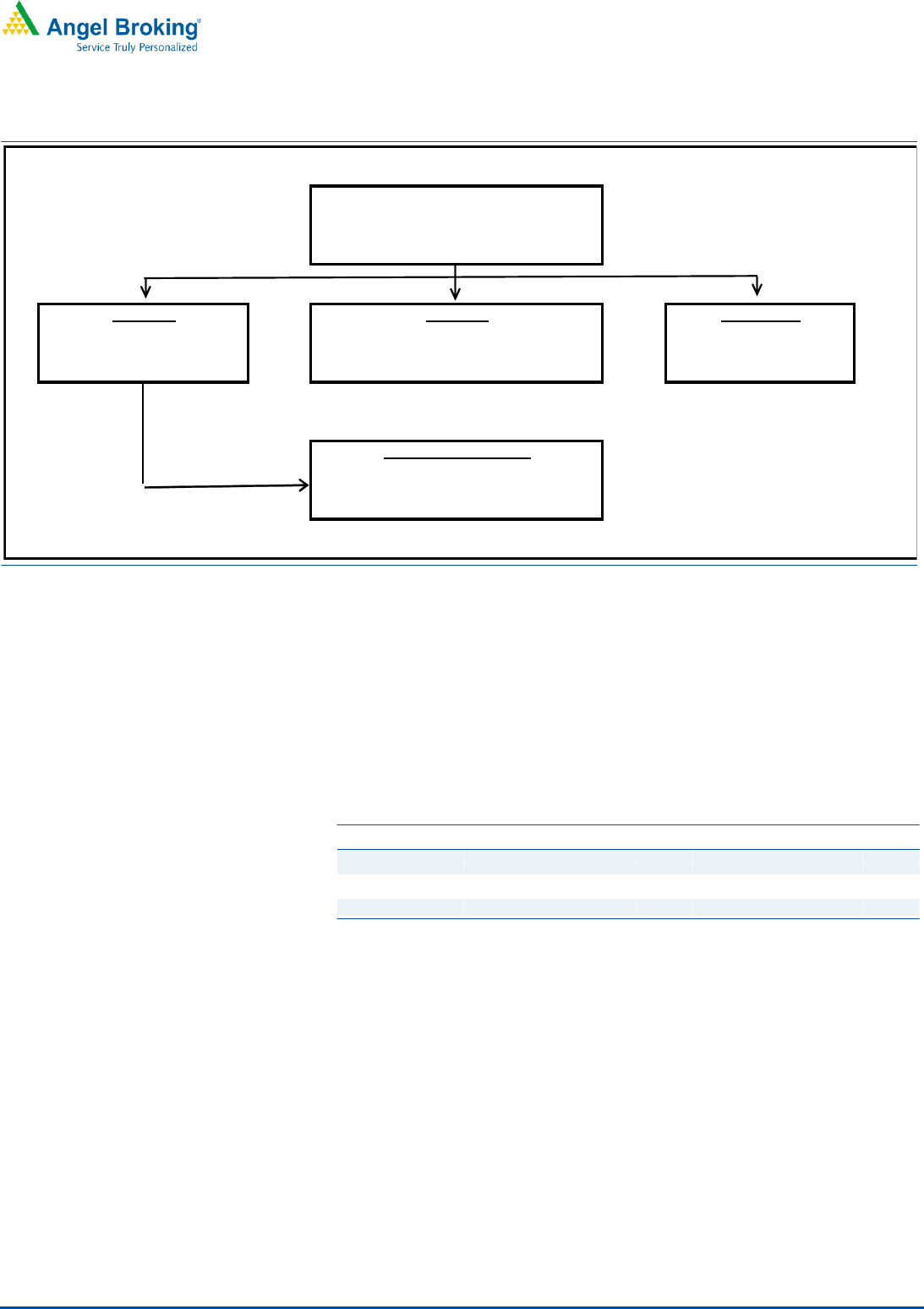

Exhibit 1: Corporate Structure

Source: Company, Angel Research

Issue details

The company is raising `151.2cr through a fresh issue of equity shares in the price

band of `205-210. The fresh issue will constitute ~20% of the post-issue paid-up

equity share capital of the company, assuming the issue is subscribed at the upper

end of the price band. The company is offering 0.29cr shares that are being sold

by the promoter group.

Exhibit 2: Pre and Post-IPO shareholding pattern

No. of shares (Pre-issue)

(%)

No. of shares (Post-issue)

(%)

Promoters

2,87,96,400

99.99

2,59,16,400

71.99

Others

3,600

0.01

1,00,83,600

28.01

2,88,00,000

100

3,60,00,000

100

Source: RHP, Angel Research; Note: Calculated on upper price band

Objects of the offer

Funding future working capital requirements of the company (`63Cr will be

utilized).

Funding capital expenditure requirements of the company (`52cr will be

utilized).

General corporate purpose.

PSP Projects Inc. (100%)

Subsidiary

Subsidiary

PSP Projects and Proactive Constructions Private

Limited (74%)

Joint Venture

GDCL & PSP Joint Venture

(49% Interest)

PSP Projects Limited

Step-down Joint Venture

P & J Builders LLC (50%)

4

PSP Projects | IPO Note

May 16, 2017

4

Investment Rationale

Strong track record of successful project execution:

PSP has established a track record of successfully executing a diverse mix of

construction projects. Since incorporation in August 2008, company has executed

80 projects as of March 31, 2017, for a host of corporate, government and other

customers across diverse segments. One of the first major projects that had been

completed was the construction of the GCS Medical College, Hospital and

Research Centre (managed by the Gujarat Cancer Society) in June 2012.

Subsequently, it has successfully executed a number of prestigious projects,

including, Inter Alia, the construction and interior works of Swarnim Sankul 01 and

02 at Gandhinagar (the office of the Chief Minister and the Cabinet Ministers of

the State of Gujarat), the construction of the Zydus Hospital at Ahmedabad, and

various activitiess in relation to the Sabarmati Riverfront Development project at

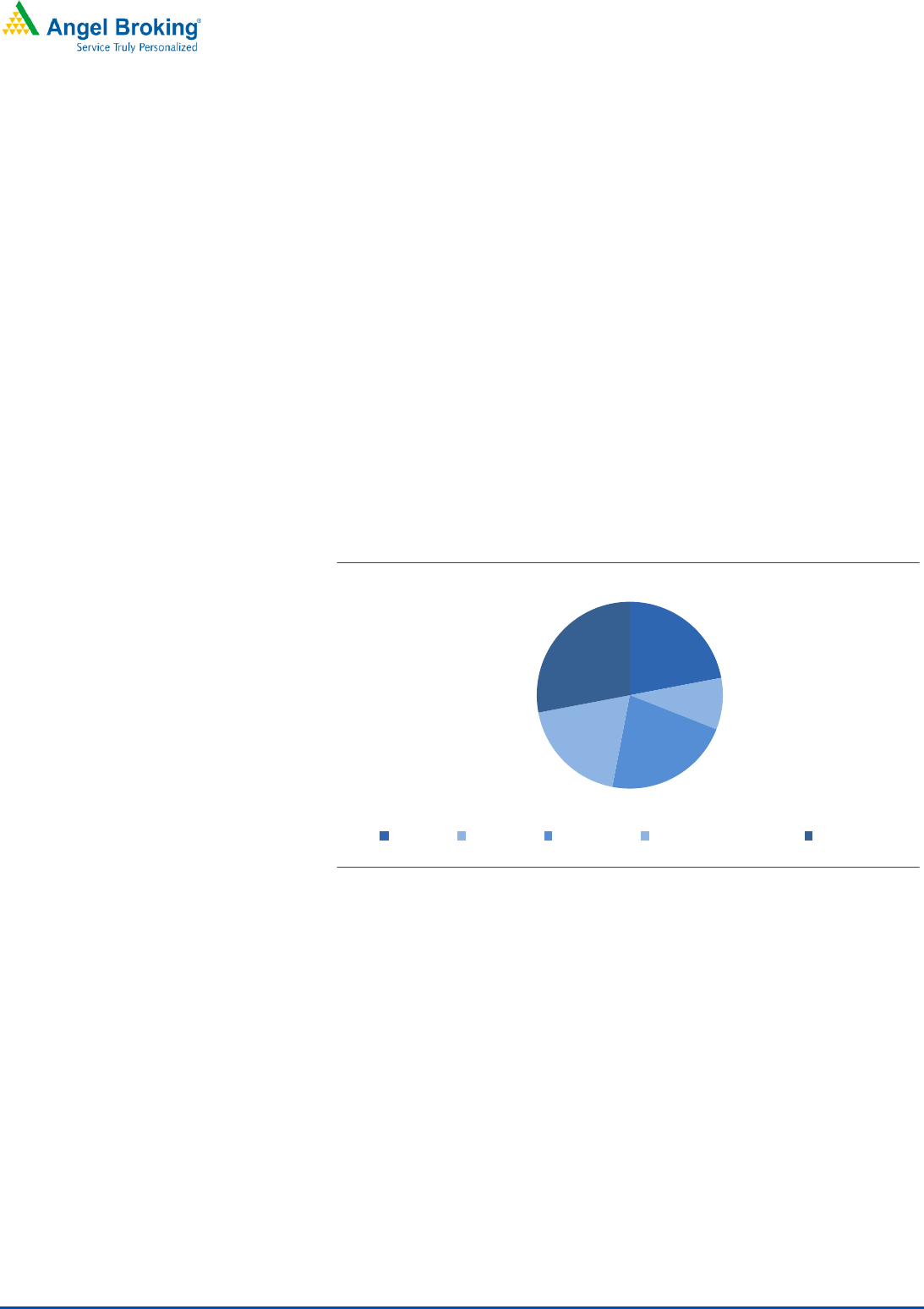

Ahmedabad. A breakdown of the Company’s aggregate contract income for the

preceding five Fiscals and the nine-month period ended December 31, 2016, on a

restated standalone basis, is represented in the chart below:

Exhibit 3: Breakup of Contract Income

Source: Company, Angel Research

The Company’s standalone total order book as of March 31, 2017, was `729.2cr,

which comprised of 17 institutional projects, four industrial projects, four

government projects and two government residential projects.

PSP believes that its experienced management skills and execution teams give it a

competitive advantage and has contributed significantly in increasing company’s

project execution capabilities. Over the years, PSP has developed its capabilities

across various stages of a typical project life cycle, commencing from business

development, tendering, engineering and design, procurement and construction.

This has also helped build expertise in executing projects across a wide range of

segments such as the construction of manufacturing and processing facilities,

hospitals, government buildings, educational institutes, corporate offices and

residential buildings, which in turn, enables it to diversify its order book and

reduces its dependence on any one sector or type of project. Company believes

that over the years, it has developed a reputation for undertaking challenging and

22%

9%

22%

19%

28%

Industrial

Residential

Government

Government Residential

Institutional

5

PSP Projects | IPO Note

May 16, 2017

5

diverse projects in a timely manner, which is reflected by track record of project

execution and long-standing relationships with a number of key customers.

Long-standing relationships with customers

Company believes that its reputation for completing projects in a timely manner

and focus on quality has helped build strong relationships with its customers. PSP

has completed or is currently undertaking projects for a number of reputed

customers, including, Inter Alia, Cadila Healthcare Limited, Care Institute of

Medical Sciences Limited (CIMS), Claris Injectables Limited, Emcure

Pharmaceuticals Limited, Gelco Electronics Private Limited, GCS Medical College,

Hospital and Research Centre (managed by the Gujarat Cancer Society), the

Government of Gujarat (through the Executive Engineer, Capital Project Division),

Inductotherm (India) Private Limited, Intas Pharmaceutical Limited, Kaira District

Co-operative Milk Producers’ Union Limited (Amul Dairy), KHS Machinery Private

Limited, Nirma Limited, Sabarmati River Front Development Corporation Limited,

Torrent Pharmaceuticals Limited and WTC Noida Development Company Private

Limited.

Further, Company has received additional projects from several of its customers

despite increased competition in the region within which the company operates.

For example, since incorporation in Fiscal 2009, PSP has executed 14 projects for

Cadila Healthcare Limited and its affiliates, six projects for Torrent Pharmaceuticals

Limited and its affiliates and four projects for Nirma Limited and its affiliates.

Further, company has also executed various works in relation to the Sabarmati

Riverfront Development project at Ahmedabad for the Sabarmati River Front

Development Corporation Limited. PSP believes that its experienced management

team and specifically, Chairman and Managing Director and CEO, Prahaladbhai

Shivrambhai Patel, has been instrumental in establishing and preserving these

customer relationships. Company intends to continue to leverage these long-

standing relationships and continue to grow its business operations in the future.

Leveraging position as a rapidly growing construction company in Gujarat

PSP is a rapidly growing construction company based in Gujarat, and intends to

establish itself as one of the leading construction companies in the state. As per the

Restated Standalone Financial Statements, the Company’s contract income has

grown from `178.2Cr in FY2012 to `454.2Cr in FY2016, at a CAGR of 26.35%,

and the Company’s profit after tax, as restated, has increased from `8.4cr in

FY2012 to ` 24.9cr in FY2016, at a CAGR of 31.44%. Further, as per the Restated

Standalone Financial Statements, the Company’s contract income for the nine

months ended December 31, 2016, was ` 23.9Cr, and the Company’s profit after

tax, as restated, was `21.5Cr. Company intends to continue to focus on

undertaking industrial, institutional and government projects in Gujarat, where it

believes it has an established reputation associated with quality and a track record

of successful execution. As of March 31, 2017, 70.20% of the Company’s total

order book consisted of projects that we are executing in Gujarat. Company

believes that economic growth in Gujarat is expected to result in an increased

demand for government and infrastructure, industrial, residential and commercial

6

PSP Projects | IPO Note

May 16, 2017

6

projects. Thus, company intends to continue to leverage its growth and increased

execution capacities to consolidate its position in the Gujarat market.

Augment customer relationships and optimize project mix

Company intends to further develop its long-standing customer relationships by

providing high quality services with the same amount of dedication as it had in the

past. Through its robust systems and capable project management teams,

company intends to closely monitor client satisfaction and be responsive to its

evolving needs. PSP believes that completing customers projects in a timely manner

whilst upholding the highest-standards of quality, is the most effective manner in

which companies can develop and maintain strong relationships with its

customers. Thus, PSP intends to strive to exceed client expectations during every

stage of the project life cycle.

To improve profitability and cash flows, company intends to select its future

projects carefully and optimize its client mix. Over the years, the scale and

complexity of projects has gradually increased and PSP seeks to continue to focus

on projects with higher contract value. Further, PSP believe that its financial

strength also enables it to access additional bank financing, which in turn, will

allow it to bid for larger and more prestigious projects, with opportunities for

potentially higher margins. Going forward, company intends to actively access

such opportunities to bid for larger and more prestigious projects, with

opportunities for potentially higher margins.

Expanding geographical footprint

PSP intends to expand its geographical footprint and grow its business by

increasing orders from beyond Gujarat. To control diversification risks, PSP may at

first, limit its expansion to other states for undertaking projects first in the areas

where its core competencies lie. Through an increasingly diversified portfolio,

company hopes to broaden its revenue base and also hedge against risks in

specific areas or projects and protect themselves from fluctuations resulting from

business concentration in limited geographical areas. With increased experience

and success, however, company’s rate of expansion may increase in terms of

increases in the number of new states and projects it undertakes. In FY2017, the

Company was awarded projects in Bangalore, Karnataka, in Churu, Rajasthan,

and in Udaipur, Rajasthan and the aforesaid projects constituted 11.56%, 8.39%

and 9.85%, respectively, of the Company’s total order book as on March 31,

2017. The Company has also bid for projects in Kochi, Kerala, Hyderabad,

Telangana and Udaipur, Rajasthan.

PSP believes that geographical diversification of projects will reduce its reliance on

home state of Gujarat and allow it to capitalise on different growth trends in

different states across the country.

Experienced management and promoter

Company has a qualified and dedicated management team, which is led by

Chairman and Managing Director and CEO, Prahaladbhai Shivrambhai Patel,

7

PSP Projects | IPO Note

May 16, 2017

7

who is also one of Promoters. Immediately prior to the incorporation of the

Company, Prahaladbhai Shivrambhai Patel, had been carrying on the business of

civil construction by way of a proprietorship firm, namely BPC Projects, whose

business was taken over by the Company in 2009. Company believes that

Prahaladbhai Shivrambhai Patel, who has over 30 years of experience in the

business of construction, has played a significant role in the development of its

business, and benefited from his technical expertise, industry knowledge and

customer relationships. Further, management team also comprises of a number of

qualified, experienced and skilled professionals, who have several years of

experience across various sectors.

Company believes that its management team has been instrumental in the growth

of its business operations, customer relationships and reputation. Further,

company believes that management team’s collective experience and execution

capabilities enables it to understand and anticipate market trends, manage the

growth and expansion of its business operations, and respond to trends in design,

engineering and construction of projects based on the preferences of its customers.

Company will continue to leverage on the experience of management team and

their understanding of the construction market, particularly in the areas where

company operates and proposes to operate, to take advantage of current and

future market opportunities.

8

PSP Projects | IPO Note

May 16, 2017

8

Outlook and Valuation

In terms of valuation, PSP’s P/BV multiple annualised 9MFY2017 at 7.9x, works

out to be at premium to peers (Ahluwalia Contracts 5.2x, Nila Infra. 3.3x, JMC

projects 1.4x, Prakash Controwell 0.4x, RPP Infra 3.7x). Moreover, PSP is aspiring

to get in the higher ticket size projects, which is dominated by well reputed players.

Management’s lack of experience in diverse geographies and lack of visibility of

future order book may become a cause of concern for growth strategy. Hence, we

recommend NEUTRAL rating on the issue.

Key risks

Currently there are outstanding legal proceedings involving PSP. Any adverse

decision may render it liable to liabilities and may adversely affect its business,

operations and profitability.

Company sources a large part of new orders from its relationships with

corporate and other customers, both present and past. Any failure to maintain

long-standing relationships with existing customers or forge similar

relationships with new ones would have a material adverse effect on

company’s business operations and profitability.

If the company is not successful in managing its growth, company’s business

may be disrupted and profitability may be reduced.

9

PSP Projects | IPO Note

May 16, 2017

9

Consolidated Income Statement

z

Y/E March (Rs cr)

FY2013

FY2014

FY2015

FY2016

9MFY17

Total operating income

257

210

280

476

279

% chg

44.0

(18.2)

33.3

69.7

-

Total Expenditure

235

194

258

441

247

Cost of materials consumed

98

80

132

206

102

Construction & Subcontracting Expenses

119

95

93

205

119

Personnel

6

11

24

14

14

Others Expenses

12

8

9

16

11

EBITDA

22

17

22

35

32

% chg

42.6

(23.8)

33.9

55.9

(% of Net Sales)

8.5

8.0

8.0

7.3

11.5

Depreciation& Amortisation

4

4

5

7

6

EBIT

18

13

17

27.8

26

% chg

45.1

(28.3)

31.8

61.3

(% of Net Sales)

7.1

6.2

6.1

5.8

9.4

Interest & other Charges

4

2

2

4

6

Other Income

4

4

7

10

10

(% of PBT)

20.5

28.4

30.6

28.9

34.0

Exceptional Items

-

-

-

-

-

Recurring PBT

18

15

21

34

31

% chg

(15.3)

38.0

59.5

Tax

6

5

7

12

10

PAT (reported)

12

10

14

22

21

% chg

(17.8)

39.6

55.3

(% of Net Sales)

4.8

4.8

5.0

4.6

7.4

Basic & Fully Diluted EPS (Rs)

4.3

3.5

4.9

7.9

7.2

% chg

(17.7)

39.4

60.8

10

PSP Projects | IPO Note

May 16, 2017

10

Consolidated Balance Sheet

Y/E March (` cr)

FY2013

FY2014

FY2015

FY2016

9MFY17

SOURCES OF FUNDS

Equity Share Capital

1

1

1

3

29

Reserves& Surplus

26

34

46

61

56

Shareholders Funds

27

35

47

64

85

Minority Interest

-

-

-

0

0

Total Loans

13

25

33

46

86

Deferred Tax Liability

-

-

-

-

-

Total Liabilities

40

60

80

110

171

APPLICATION OF FUNDS

Net Block

18

19

33

54

53

Capital Work-in-Progress

-

-

0

-

-

Investments

3

9

13

14

17

Goodwill

-

-

-

0

0

Current Assets

79

109

140

183

222

Inventories

2

2

4

10

19

Sundry Debtors

12

14

24

20

13

Cash

45

68

85

112

145

Loans & Advances

16

19

14

27

33

Other Assets

4

6

13

14

12

Current liabilities

61

76

107

143

125

Net Current Assets

18

32

33

40

97

Deferred Tax Asset

0

0

0

2

3

Mis. Exp. not written off

-

-

-

-

-

Total Assets

40

60

80

110

171

Source: Company, Angel Research

11

PSP Projects | IPO Note

May 16, 2017

11

Consolidated Cash Flow Statement

Y/E March (Rs cr)

FY2013

FY2014

FY2015

FY2016

9MFY17

Profit before tax

18

15

21

34

31

Depreciation

4

4

5

1

6

Change in Working Capital

10

8

15

55

(25)

Interest / Dividend (Net)

0

0

0

0

0

Direct taxes paid

(5)

(5)

(7)

42

(10)

Others

(0)

(2)

(5)

(132)

(5)

Cash Flow from Operations

26

20

30

0

(4)

(Inc.)/ Dec. in Fixed Assets

4

(4)

3

(27)

7

(Inc.)/ Dec. in Investments

(2)

(37)

(28)

27

(16)

Cash Flow from Investing

2

(41)

(26)

0

(9)

Issue of Equity

4

4

6

(27)

8

Inc./(Dec.) in loans

0

0

(0)

(0)

(1)

Others

(17)

5

(2)

29

29

Cash Flow from Financing

(14)

9

4

1

36

Inc./(Dec.) in Cash

15

(12)

8

1

23

Opening Cash balances

69

84

72

82

82

Closing Cash balances

84

72

81

84

105

Key Ratios

Y/E March

FY2013

FY2014

FY2015

FY2016

Valuation Ratio (x)

P/E (on FDEPS)

49.2

59.8

42.9

26.7

P/CEPS

37.8

44.0

31.5

20.9

P/BV

22.7

17.4

12.9

9.5

EV/Sales

2.2

2.6

1.9

1.1

EV/EBITDA

25.9

33.0

24.1

15.0

EV / Total Assets

14.3

9.2

6.8

4.8

Per Share Data (Rs)

EPS (Basic)

4.3

3.5

4.9

7.9

EPS (fully diluted)

4.3

3.5

4.9

7.9

Cash EPS

5.5

4.8

6.7

10.1

Book Value

9.2

12.1

16.3

22.2

Returns (%)

ROCE

45.7

21.8

21.6

25.4

ROE

46.1

28.9

30.0

34.2

Turnover ratios (x)

Inventory / Sales (days)

3

3

5

8

Receivables (days)

17

24

31

16

Payables (days)

50

69

82

63

Note: Valuation ratios based on pre-issue outstanding shares and at upper end of the price band

12

PSP Projects | IPO Note

May 16, 2017

12

Research Team Tel: 022 - 39357800 E-mail: research@angelbroking.com Website: www.angelbroking.com

DISCLAIMER

Angel Broking Private Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited,

Bombay Stock Exchange Limited and Metropolitan Stock Exchange Limited. It is also registered as a Depository Participant with CDSL

and Portfolio Manager with SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Private Limited is a

registered entity with SEBI for Research Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number

INH000000164. Angel or its associates has not been debarred/ suspended by SEBI or any other regulatory authority for accessing

/dealing in securities Market. Angel or its associates/analyst has not received any compensation / managed or co-managed public

offering of securities of the company covered by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should

make such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the

companies referred to in this document (including the merits and risks involved), and should consult their own advisors to determine

the merits and risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any.

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Pvt. Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Pvt. Limited has not independently verified all the information contained within this document. Accordingly, we cannot

testify, nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document.

While Angel Broking Pvt. Limited endeavors to update on a reasonable basis the information discussed in this material, there may be

regulatory, compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Pvt. Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from

or in connection with the use of this information.